The aim of this case is to underscore the importance of price forecasting through the observation of market trends. Traders, armed with varying information and perspectives about the market index movement from their analysts’ reports, leverage these insights in forecasting the expected returns of all available tradable securities. They construct algorithmic investment strategies by comparing predicted future prices with current market prices.

During the trading simulation, participants receive multiple pieces of information from their private analysts outlining expectations for future market index prices. At the case’s outset, traders are informed about beta coefficients, which measure the volatility of each security relative to the overall market. This aids in the initial identification of assets’ correlation or sensitivity to the market index. Since the beta coefficient is contingent upon market movement, it varies over time.

After receiving forecasted market price information, traders must incorporate their computed expected return on the market index and dynamic beta into a simple predictive model. This model helps anticipate future price movements in each tradable security. Utilizing the CAPM model, known for its predictive power in estimating asset returns, traders employ algorithms to predict future expected returns for each security and build investment strategies aimed at yielding increased profits.

Traders use private analysts’ information to compute the expected return from the overall market. Then, by applying beta coefficients, they forecast the potential return from a range of stocks. It’s crucial to acknowledge that analysts’ predictions may not be entirely precise in forecasting market index prices. Hence, participants need to account for a certain margin of error in their asset return calculations, assuming this margin of error adheres to a standard normal distribution.

This case imposes restrictions on the trading positions traders may take, including long or short positions, with penalties for exceeding predefined trading limits. Additionally, submitting substantial orders can significantly deviate market prices from analysts’ forecasts, influencing the prediction of future returns and the subsequently developed strategies. Traders can secure profits by placing limit or market orders based on their forecasted price outcomes.

OBJECTIVES

Objective 1

Develop a forecasting algorithm model using the provided template to assess the influence of private news on the future prices of both the market index and individual stocks. Explore the utilization of tick-by-tick historical last prices to gauge the sensitivity of stock prices to market risk. Integrate this data into the CAPM model to predict future stock price movements.

Objective 2

Construct a trading algorithm designed to identify profitable investment opportunities by forecasting future returns earned on individual tradable stocks. Compare these forecasts across the available stocks to pinpoint potentially profitable investment avenues.

MARKET DYNAMICS

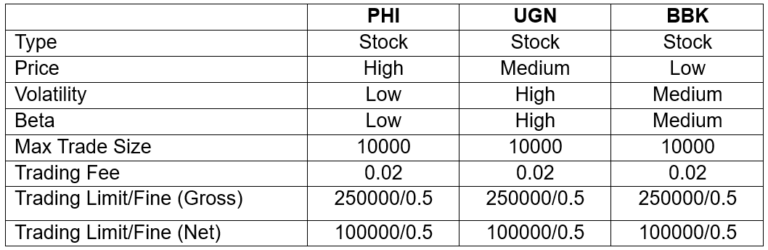

ALGO Forecasting Simulation accounts for one-quarter of the trading activities involving three specific stocks: Platinum Holding Inc. (PHI), Upper Green Corporation (UGN), and Branded Blocks (BBK).

This simulation spans a 3-month duration, running for a period of 10 minutes, equivalent to 600 ticks, with 50 ticks representing one week of trading. At tick 1, participants receive news that provides insights into the risk-free rate based on the 10-year Government bond yield, along with the initial beta coefficients of each stock. This information helps them to identify the potential excess returns they can earn in contrast to the market premium.

On a weekly basis, private information will be sent about the forecasted future price on the Global Market Index (GLX). Over the course of the simulation, a total of 12 private news updates will be released at various points during each week, containing information on the anticipated GLX price for the upcoming day.

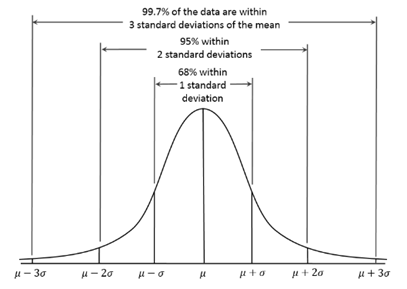

Participants can utilize this information to compute the future return on the market index and subsequently employ it to make predictions about the future prices of securities as accurately as possible. The accuracy of these predictions is contingent upon the margin of error associated with the analyst’s forecast for the market index price. For the purposes of our model, let’s assume that this margin of error, denoted as X, follows a standard normal distribution as outlined below:

For instance, a perfect forecast of the market price implies that the margin of error will be minimal, approaching zero. There is a 99.7% likelihood that the error falls within the 3 standard deviations from the mean of the error distribution.

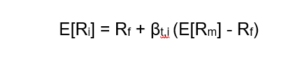

Participants can use the expected market return along with their estimated time-varying beta within the fundamental CAPM model to project the expected return from a particular stock. The basic CAPM[1] model is represented by the following equation:

[1] It does not say which asset is under-performing or over-performing with respect to the benchmark market index.

where:

E[Ri] is the expected return of investment on stock i

Rf is the risk-free rate

ꞵt,i is the beta of stock i at time t

Rm is the forecasted market return on GLX

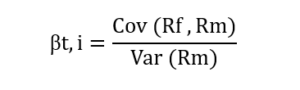

To calculate beta sensitivity of the stock, participants must capture the historical prices of all the assets. News will start appearing from tick 30. Participants can collect the historical price from the beginning and estimate beta using the following function:

1 – It does not say which asset is under-performing or over-performing with respect to the benchmark market index.

Alternatively, beta is equal to the slope coefficient when the historical return of market index is regressed on the historical returns of a stock.

The expected return predicted by the CAPM model serves as a tool for participants to discern potential price movements in each tradable security. Participants can then build investment strategies by comparing the predicted price with the market price and conducting risk-return analysis across all stocks. The forecasted price can be employed to generate profits through the submission of limit or market orders. However, one should avoid following market-making strategies and submitting large orders, as these actions can cumulatively impact asset prices and indirectly influence the investment strategies derived from predictive analysis.

Participants need not be concerned about the liquidity of the securities, as computer-generated traders will continuously place buy and sell orders, marked as “ANON” in the order book. The parameters are calibrated to meet specific market requirements, and these computer traders operate without knowledge of future asset price movements. As a result, they place buy and sell orders with equal probability and prices that are randomly generated, following a normal distribution centered around the mid-market price.

Furthermore, there is a trading limit of 250,000 shares gross and 100,000 shares net, signifying that once this limit is exceeded, participants will be unable to execute additional trades, and a penalty of 50 cents per share will be incurred. The maximum order size for any single order, whether long or short, is capped at 10,000 shares. Additionally, a commission of 2 cents per share is levied on every transaction involving PHI, UGN, and BBK.

Participants have the flexibility to choose between utilizing either the REST or the VBA API for their trading activities. The system enforces a maximum of 500 orders per second to maintain orderly market operations.