General Information

Target Audience

The course learning objectives have general applicability, but are particularly relevant for developing skills for risk management, investment strategies, and securities trading. This course is a supplemental course for both the Data Analytics & Modeling and Finance emphases.

Format

12 weekly sessions plus optional Q&A sessions prior to course deliverables.

Course Mission

- Reviewing recent innovations in financial markets and securities, information processing, etc.

- Developing modeling skills (e.g. coding, algorithms, Monte Carlo simulation, etc.)

- Practicing decision making for investment, trading, and risk management strategies

Course Scope

We will use probabilistic modeling and stochastic simulation as tools for guiding risk-informed decisions in complex environments with material uncertainty about the future. The RIT Market Simulator platform (order-driven market/matching engine) and the associated real-time RIT Decision Cases facilitate deriving robust strategies for the decisions that arbitrageurs, portfolio and risk managers make in real time, including managing liquidity risk, market risk, crash risk, model risk and real economy risks.

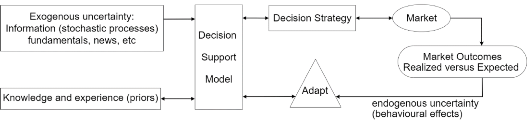

Schematic of the simulation-based learning approach using the RIT Decision Cases:

Evaluation and Grade Breakdown

| Component | Due Date | Weight |

|---|---|---|

| Individual & Group Decision Case Reports | See course outline | 34% |

| Pre-Class (Open Book) Quizzes & Final Quiz | Ongoing and April 8 in class | 36% |

| Decision Performance & Participation | See course outline | 30% |

Required Resources

All course resources (case briefs, decision support models, tutorials, background reading) available online.